Solar Loan Calculator: South Africa's 2026 Guide

A solar loan calculator is a tool that computes your monthly repayment and total loan cost based on your system price, interest rate, and loan term. South African homeowners using one can assess whether solar installation funding fits their budget before signing anything. Specialized solar loans in 2026 carry interest rates from 6.99% to 9.99% APR with repayment terms between 5 and 25 years. That range means your monthly payment on the same R150,000 system could vary by thousands of rands depending on the term you choose. The federal residential solar tax credit expired on December 31, 2025, so South African homeowners financing through loans in 2026 no longer have that buffer to reduce their effective cost. Running accurate numbers before you commit is not optional. It is the difference between a manageable monthly payment and a financial strain that lasts a decade.

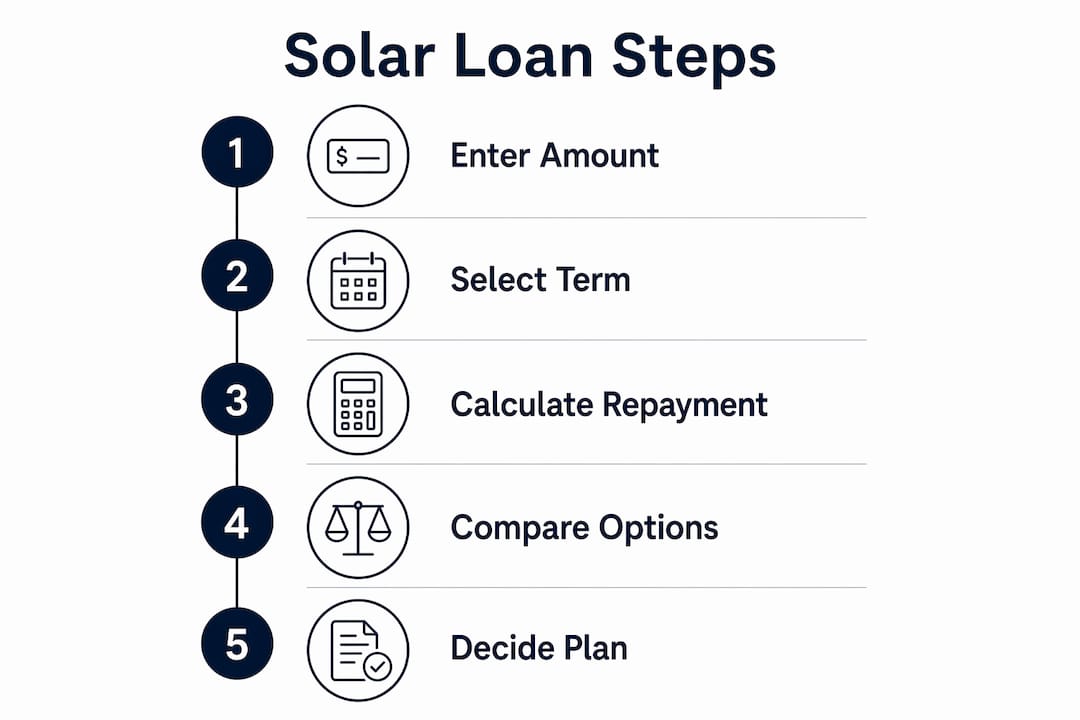

How does a solar loan calculator work?

A solar loan calculator applies an amortized loan formula to your inputs and returns a monthly payment figure. The standard formula is: Monthly Payment = Principal × [r(1+r)^n] ÷ [(1+r)^n − 1], where r is the monthly interest rate and n is the total number of payments. That formula is the same one banks use for home loans and vehicle finance, applied here to your solar system cost.

The inputs you need to run an accurate calculation include:

- Loan amount (principal): The total financed amount, which is the system cost minus any down payment, plus dealer fees.

- Annual interest rate (APR): The rate your lender quotes, expressed as a percentage. Divide by 12 to get the monthly rate.

- Loan term: The repayment period in months. South African solar loans typically run 60 to 300 months (5 to 25 years).

- Dealer fees: A charge some lenders add to the principal, often 20–30% of the cash price, to buy down the advertised interest rate.

- Down payment: Any upfront amount you pay, which reduces the financed principal directly.

South African solar loans are mostly unsecured personal loans, meaning your home is not used as collateral. That structure leads to higher interest rates compared to secured products like home equity lines of credit. It also means faster approval, which suits homeowners who need backup power quickly during load shedding.

The calculator's output tells you three things: your fixed monthly repayment, the total interest you will pay over the loan life, and the overall cost of the system including financing. Comparing that monthly figure to your current Eskom bill is the first real affordability test.

Pro Tip: Always enter the financed principal, not the advertised system price. If a lender adds a dealer fee to the loan, your actual principal is higher than the quote on the installer's invoice.

Pro Tip: Always enter the financed principal, not the advertised system price. If a lender adds a dealer fee to the loan, your actual principal is higher than the quote on the installer's invoice.

Step-by-step guide to using a solar payment estimator

Getting accurate results from a solar payment estimator requires clean inputs. Garbage in, garbage out. Follow these steps to get numbers you can actually use.

- Gather your current electricity costs. Pull your last three Eskom or municipal bills and calculate your average monthly spend. This is your baseline. Your loan repayment needs to compare favorably to this number, at least over the medium term.

- Get at least two solar installation quotes. Contact verified installers and request itemized quotes showing the cash price of the system separately from any financing fees. Solarza connects South African homeowners with vetted local installers across all nine provinces, making this step faster.

- Confirm the financed principal. Ask each lender to state the exact amount being financed, including all dealer fees. This is the number you enter as your principal in the calculator, not the system's cash price.

- Enter the APR and loan term. Use the annual percentage rate from the loan offer. Try multiple term scenarios: 5 years, 10 years, and 20 years. Watch how the monthly payment drops as the term extends, and watch how the total interest climbs.

- Check all three outputs. Record the monthly payment, total interest paid, and total loan cost for each scenario. A 20-year term on a R150,000 loan at 9% APR produces a lower monthly payment than a 5-year term, but the total interest cost is dramatically higher.

- Compare the monthly payment to your electricity bill. Without the federal tax credit, your loan payment in 2026 may initially match or exceed your current electricity bill. The financial case builds over time as utility rates rise and your loan payment stays fixed.

- Use the results to negotiate. If one lender's total cost is significantly higher than another's, you have a concrete number to push back with. Lenders expect negotiation.

Pro Tip: Use Solarza's solar savings calculator to estimate how much your system will generate before you run the loan numbers. Knowing your projected savings makes the repayment comparison far more meaningful.

Common mistakes to avoid when you calculate solar loan payments

Most homeowners make at least one of these errors when they first calculate solar loan payments. Each one can distort your results enough to lead to a bad decision.

- Ignoring dealer fees. Many lenders advertise a low APR but embed a dealer fee of 20–30% of the cash price into the principal. A R100,000 system can become a R125,000 loan before you notice. Always ask for a full principal breakdown in writing.

- Expecting a tax credit that no longer exists. The Section 25D federal residential solar tax credit expired on December 31, 2025. Homeowners who factor a 30% tax credit into their affordability math in 2026 are working with a number that no longer applies.

- Confusing APR with total cost. A low APR does not mean a low total cost. A 7% APR over 25 years costs more in total interest than a 9.5% APR over 7 years. Always compare total loan cost, not just the rate.

- Overlooking prepayment penalties. Some solar loans include clauses that penalize early repayment or trigger re-amortization if you pay a lump sum. Read the fine print before you sign.

- Not shopping multiple lenders. Getting full loan details in writing, including the amortization schedule and all fees, from at least three lenders is the only way to know whether you are getting a fair deal.

- Ignoring future electricity rate increases. Your loan payment is fixed. Eskom tariffs are not. A repayment that feels tight today may feel comfortable in five years as your electricity savings grow.

"A solar loan calculator is a planning tool. The real APR and terms vary by credit score and market conditions, so always use multiple quotes when deciding." — Solar Bid Analyzer

How to interpret your solar financing calculator results

Your solar financing calculator produces numbers. Interpreting those numbers correctly is where most homeowners need help.

Monthly payment vs. monthly savings

The first comparison is simple: does your projected monthly loan repayment exceed your current electricity bill? If it does, you are cash-flow negative from day one. That is not automatically a dealbreaker. Electricity tariffs in South Africa rise consistently, and your loan payment stays fixed. Over a 10-year period, a repayment that starts above your current bill often ends up well below what you would have paid Eskom. Longer loan terms reduce monthly payments but raise total interest costs significantly. That trade-off is the central tension in every solar financing decision.

Loan ownership vs. leasing or PPAs

A loan gives you full ownership of the system. That matters for two reasons. First, a owned solar installation increases your property's market value. Second, you capture all the electricity savings directly. Leases and power purchase agreements (PPAs) keep the system in the provider's name. In 2026, solar leases and PPAs remain attractive because providers can access commercial tax credits that individual homeowners cannot. That means lease providers can sometimes offer lower monthly payments than a loan buyer can achieve. The trade-off is that you do not own the system and you do not build equity.

Comparing financing options side by side

| Financing factor | Solar loan | Lease or PPA |

|---|---|---|

| System ownership | Homeowner | Provider |

| Monthly payment structure | Fixed repayment | Fixed or variable rate |

| Long-term savings potential | Higher (you own the output) | Lower (provider captures credits) |

| Property value impact | Positive | Minimal or disputed |

| Flexibility to sell home | Full control | Transfer or buyout required |

| 2026 tax credit access | None (expired) | Provider may access commercial credits |

The best solar financing option in 2026 depends on your credit score, cash flow priorities, and how long you plan to stay in the property. No single answer fits every homeowner.

Key Takeaways

A solar loan calculator is the most reliable way for South African homeowners to compare financing options accurately, avoid hidden costs, and make a confident decision about solar installation funding in 2026.

| Point | Details |

|---|---|

| Use the financed principal, not the cash price | Dealer fees of 20–30% inflate the loan amount beyond the advertised system price. |

| The federal tax credit expired in 2025 | Homeowners financing solar in 2026 must calculate affordability without a 30% credit offset. |

| Compare total cost, not just monthly payment | Longer terms lower monthly payments but increase total interest paid significantly. |

| Loans give ownership; leases do not | A solar loan builds equity and raises property value; a lease or PPA keeps the system in the provider's name. |

| Always get multiple loan offers in writing | APR, fees, and terms vary enough between lenders to change your total cost by tens of thousands of rands. |

What I have learned from watching homeowners use solar calculators

Most homeowners treat a solar loan calculator like a final answer. It is not. It is a planning tool, and the gap between a calculator estimate and the actual loan offer can be significant depending on your credit profile and the lender's fee structure.

The detail that catches people off guard most often is the dealer fee. A homeowner sees a R120,000 system quote and enters R120,000 into the calculator. But the lender has added a R28,000 dealer fee to buy down the advertised rate. The actual loan is R148,000. The monthly payment the calculator showed was never real.

The expiration of the federal residential solar tax credit at the end of 2025 has also changed the math in ways many homeowners have not absorbed yet. Financing decisions that made sense in 2024 with a 30% credit factored in look different in 2026 without it. Leases and PPAs have quietly become more competitive for homeowners who prioritize lower monthly payments over ownership.

My advice is to run the calculator first, then get three written loan offers, then run the calculator again with the real numbers from each offer. The comparison at that stage is where the decision actually lives. Pair that process with a conversation with a vetted installer who understands local financing options. Solarza's platform makes finding those installers straightforward, and their solar cost estimator gives you a realistic system price before you approach any lender.

— Nkosi

Solarza helps South African homeowners find the right solar financing

Calculating your loan is step one. Finding a trusted installer who works with the right financing products is step two.

Solarza connects South African homeowners with verified, rated solar installers across all nine provinces. Whether you are in Johannesburg, Cape Town, or Durban, you can find installers near you and request tailored quotes that reflect real local pricing. The platform also offers a solar savings calculator to estimate your system output and monthly savings before you commit to any financing. Solarza's installer network covers panels, batteries, and inverters, giving you a complete picture of your system cost and the financing options attached to it. Request a free quote and get real numbers from vetted professionals in your area.

FAQ

What is a solar loan calculator?

A solar loan calculator is a financial tool that uses your loan amount, interest rate, and repayment term to estimate your monthly payment and total loan cost. It applies a standard amortized loan formula to help homeowners assess whether solar financing fits their budget.

What interest rates apply to solar loans in South Africa in 2026?

Specialized solar loans in 2026 typically carry interest rates between 6.99% and 9.99% APR, with terms ranging from 5 to 25 years. Rates vary based on your credit score and whether the loan is secured or unsecured.

Are solar loans in South Africa secured against my home?

South African solar loans are mostly unsecured personal loans, meaning your home is not used as collateral. This results in higher interest rates than secured products but faster approval times.

Is the federal solar tax credit still available in 2026?

No. The Section 25D federal residential solar tax credit expired on December 31, 2025. Homeowners who take out solar loans in 2026 cannot apply this credit to reduce their effective system cost.

Should I choose a solar loan or a lease in 2026?

A solar loan gives you full ownership of the system and long-term savings, while a lease or PPA may offer lower initial monthly payments because providers can access commercial tax credits. The right choice depends on your cash flow priorities, credit profile, and how long you plan to stay in the property.